Three competing open standards for AI agent payments dropped within months of each other. Stripe and Tempo launched MPP on March 18. Coinbase has x402. Google released its own scheme last September. All three use stablecoins as the default settlement layer. The winner owns a cut of every autonomous transaction on the internet, a market that runs through the $190 trillion annual cross-border payments corridor.

Current payment infrastructure was designed for humans. A checkout flow assumes someone can read a pricing page, pick a plan, enter card details, and confirm a purchase. An AI agent can't do any of that without human intervention at each step.

This isn't a hypothetical friction. Agents that need to access a dataset, spin up compute, call an API, or purchase a service are stuck. They either rely on pre-loaded credentials (brittle, scope-limited) or require a human in the loop every time money moves (defeats the point of autonomy). The agent economy needs a payment primitive that machines can call natively, the same way HTTP is a primitive for fetching data.

That's the gap all three protocols are trying to fill. They're all betting stablecoins are the answer.

MPP: Stripe builds a coalition

Stripe and Tempo co-authored the Machine Payments Protocol, an open standard that lets agents pay for services over HTTP. The mechanic is straightforward: an agent requests a resource, the server returns an HTTP 402 ("Payment Required") with a price, the agent pays in stablecoins or fiat, and retries. The whole cycle happens in seconds without human approval.

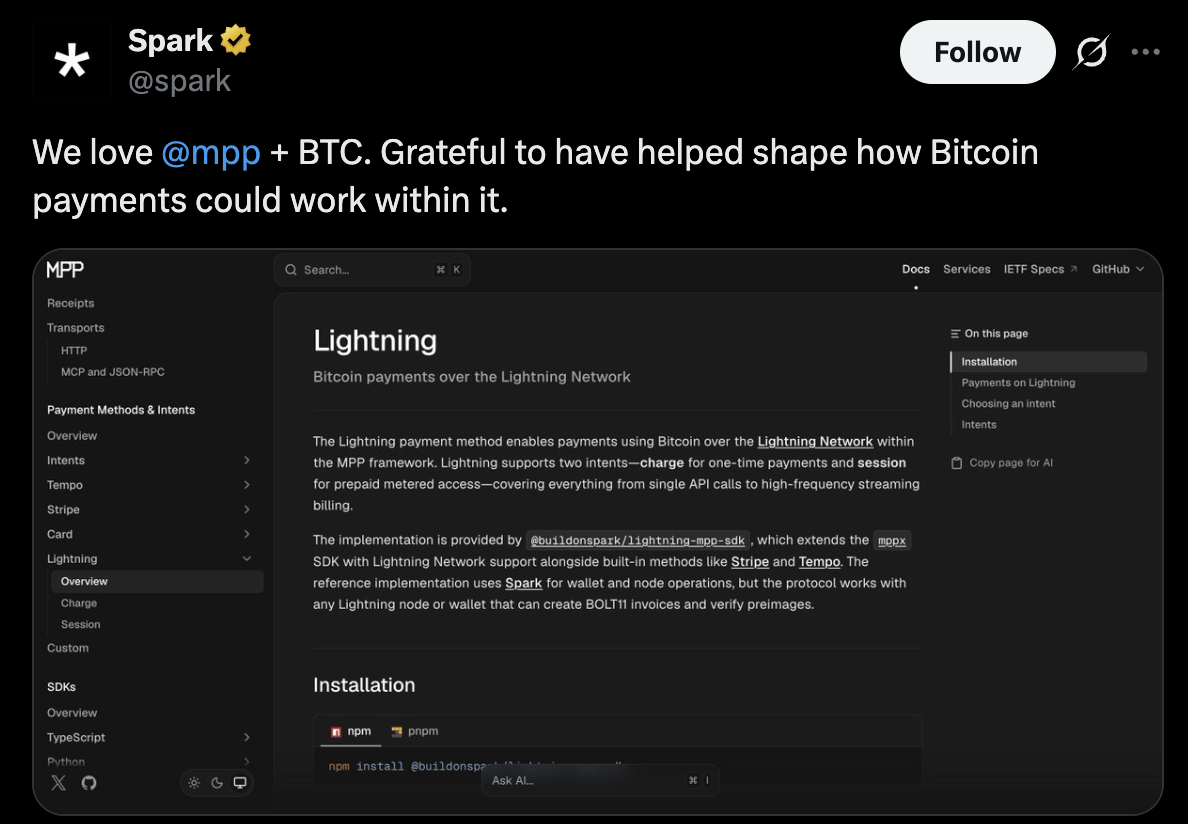

The protocol runs on Tempo's mainnet, which went live the same day, but is explicitly designed to be rail-agnostic. That's not just a design aspiration. Visa has already extended MPP to support card-based payments on its global network. Lightspark extended it to Bitcoin Lightning. Stripe extended it to cards, wallets, and BNPL via Shared Payment Tokens. Three major payment rails supporting the same protocol on day one is huge.

The sessions primitive is the most technically interesting piece. When an agent opens a session, funds are pre-authorized upfront. Payments stream continuously as the agent consumes resources, with thousands of microtransactions settling into a single on-chain transaction at the end. This matters for cost: Tempo's chain targets sub-millidollar fees and sub-second finality. Without that, every $0.001 API call becomes economically absurd to settle individually.

The launch directory already lists over 100 MPP-compatible services, including Anthropic, OpenAI, Alchemy, Dune Analytics, DoorDash, and Shopify. That's not a demo. That's a network. Design partners during the testnet phase included Mastercard, Nubank, Revolut, Standard Chartered, and Klarna, which has announced plans to issue its own stablecoin on Tempo's mainnet.

One notable constraint: stablecoin acceptance on Stripe is currently US-only. Stripe processed $1.9 trillion in total payment volume in 2025, a 34% year-on-year increase, and global stablecoin volumes doubled over the same period to $400 billion. B2B now accounts for 60% of that stablecoin volume. The infrastructure appetite is real. The regulatory runway is still being cleared.

There's also no native token. Tempo uses stablecoins for gas via an integrated AMM, and the team has explicitly cited regulatory uncertainty as the reason for not issuing a token at launch. That's a meaningful design decision. It removes speculative upside for the chain's own ecosystem but makes the pitch to Visa and Mastercard considerably cleaner.

x402: Coinbase's crypto-native challenger

Coinbase's x402 is also HTTP 402-based, the same conceptual callback to the original "Payment Required" error that web engineers reserved in 1996 and never actually used. The name is a direct reference.

The philosophical difference from MPP is origin. x402 was built from the crypto side out. It prioritizes permissionless access and crypto-native developer experience over institutional adoption. Coinbase's base is builders who are already on-chain, already holding USDC, already running agents on crypto rails.

That's a genuine advantage in parts of the market. The overlap between "developer running an AI agent" and "already has a Coinbase account" is substantial. Coinbase also has its own developer infrastructure stack, Base L2, CDP, and AgentKit, that can be composed with x402 without touching any TradFi infrastructure at all.

The tradeoff is distribution ceiling. Stripe has millions of existing merchants on PaymentIntents. A Stripe merchant can accept MPP payments with a few lines of code against infrastructure they already run. Coinbase's path to that same merchant requires a net-new integration from scratch.

Google's September scheme

Google released its agentic payments framework last September, with support for both credit cards and stablecoins. Details on adoption are thin. Google has consumer scale that neither Stripe nor Coinbase can match, and its AI stack (Gemini, Vertex) is already deployed across enterprise. If Google routes agent payments through its own protocol by default, that's a distribution play no one else can replicate.

But Google has a long history of infrastructure projects that quietly die. The protocol's survival likely depends on whether it gets embedded into Gemini's agentic stack or remains a standalone spec.

The actual battle

The protocol mechanics are similar enough that technical elegance isn't the deciding factor. All three use HTTP 402, support stablecoins, Day-1 open source. The race is network effects and distribution.

MPP has the most explicit coalition at launch: Stripe's merchant base, Visa's global card network, Lightspark's Lightning integration, and 100+ service providers in a live directory. That's a network effect argument, not a technology argument. As Visa's head of crypto Cuy Sheffield put it, MPP gives agents a clear, defined protocol for communicating with merchants. That framing isn't accidental. Visa is thinking about MPP the same way it thinks about card acceptance standards, as infrastructure that becomes default through ubiquity rather than merit.

x402's advantage is the developer community that finds anything touching Visa instinctively suspicious. There's a real cohort in CT that will route agent payments on-chain specifically to avoid TradFi rails. That's a durable base even if it stays niche.

The winner doesn't need to be singular. HTTP and HTTPS coexist. TCP/IP didn't eliminate all other networking protocols overnight. What's more likely is that MPP becomes the default for agents operating within commercial and enterprise contexts, while x402 captures the permissionless, crypto-native edge. Google's scheme captures whatever Google decides to bundle into its own agents.

What's still unresolved

Regulatory clarity on autonomous agent payments is missing globally. An agent that spends money on behalf of a user raises real questions about liability, authorization, and dispute resolution that none of these protocols address at the protocol layer. Sessions and pre-authorization help, but they don't answer the question of what happens when an agent overspends or gets exploited.

The US-only stablecoin restriction on Stripe is a real ceiling for now. Tempo targets the $190 trillion annual cross-border payment market, where correspondent banking imposes one-to-three day settlement delays. The chain's ISO 20022 compliance is designed to bridge existing bank reconciliation systems. But global stablecoin acceptance depends on regulatory progress in the EU, UK, and Asia-Pacific, none of which moves on Silicon Valley's timeline.

There's also an open question about whether Tempo's no-token design holds. Paradigm's Matt Huang said at launch that the team chose not to issue a token due to a need for greater regulatory clarity. That's a credible reason. It's also a reason that might look different in 12 months.

This stopped being a crypto story a long time ago. Stripe, Coinbase, and Google are all making the same fundamental bet. The question is which stack developers build on first, and whether the winner's network effect compounds fast enough to make the others irrelevant. Whoever wins owns a toll booth on every autonomous transaction on the internet.

If you find this helpful, feel free to follow us for future updates. ❤

PEPE0.00 -0.32%

PEPE0.00 -0.32%

TON1.25 -0.06%

TON1.25 -0.06%

BNB642.28 -0.21%

BNB642.28 -0.21%

SOL89.24 -0.27%

SOL89.24 -0.27%

XRP1.45 -0.53%

XRP1.45 -0.53%

DOGE0.09 0.42%

DOGE0.09 0.42%

TRX0.31 1.20%

TRX0.31 1.20%

ETH2144.44 -0.65%

ETH2144.44 -0.65%

BTC70565.41 1.21%

BTC70565.41 1.21%

SUI0.97 1.38%

SUI0.97 1.38%